What Is the Accounting Equation?

The accounting equation is the bedrock of all bookkeeping and financial accounting. It states:

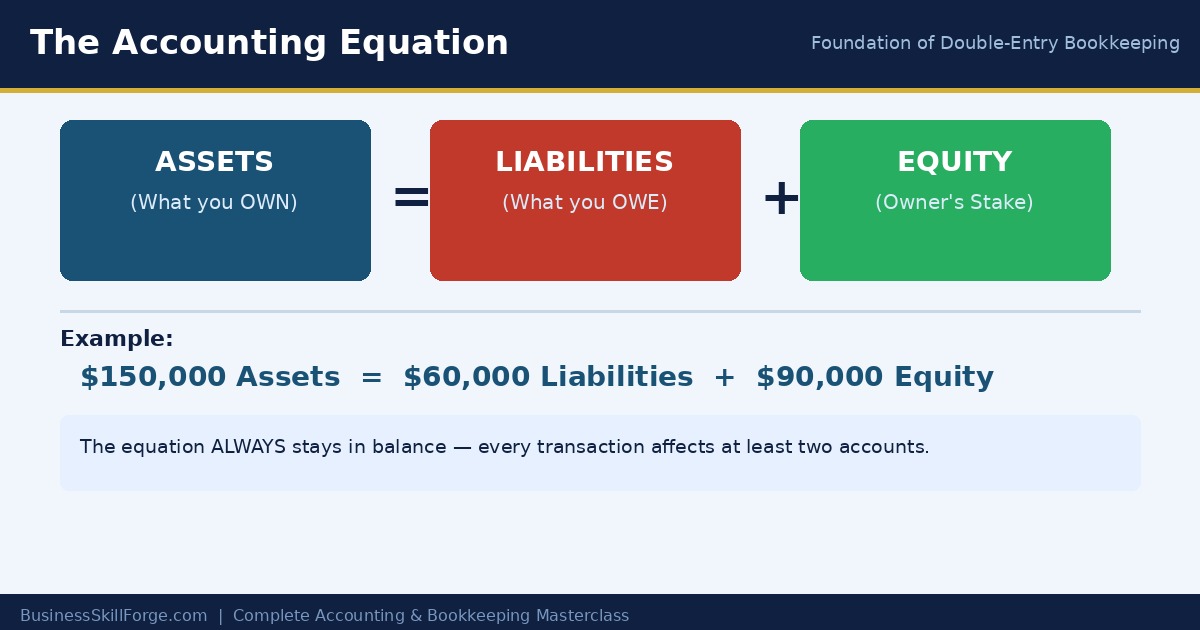

Assets = Liabilities + Owner’s Equity

Every single financial transaction that a business records must keep this equation in balance. If it ever goes out of balance, you know a mistake has been made somewhere. Think of it as the ultimate error-check in accounting.

Breaking Down Each Component

Assets — What the Business Owns

Assets are everything of value that the business owns or controls. They can be physical things you can touch, or intangible items like patents.

- Current assets — Cash, accounts receivable, inventory (expected to be used within one year)

- Non-current assets — Buildings, equipment, vehicles, long-term investments

Example: A bakery’s assets include its oven ($8,000), cash in the register ($2,000), and flour inventory ($500).

Liabilities — What the Business Owes

Liabilities are the business’s financial obligations — money it owes to other parties.

- Current liabilities — Accounts payable, short-term loans, credit card balances (due within one year)

- Non-current liabilities — Mortgages, long-term bank loans, bonds payable

Example: The bakery financed its oven with a $5,000 bank loan — that’s a liability.

Owner’s Equity — The Owner’s Stake

Equity is what’s left over for the owner after all debts are paid. It represents the owner’s claim on the business’s assets.

Equity = Assets − Liabilities

Equity increases when the business earns profit or the owner invests more money. It decreases when the business makes a loss or the owner withdraws funds (drawings).

Why the Equation Always Stays in Balance

The magic of the accounting equation is that it always balances, no matter what transaction occurs. This is because of the double-entry bookkeeping principle — every transaction has at least two effects that keep the equation balanced.

Let’s walk through three examples:

| Transaction | Assets | Liabilities | Equity |

|---|---|---|---|

| Starting position | $0 | $0 | $0 |

| Owner invests $10,000 cash | +$10,000 | — | +$10,000 |

| Balance | $10,000 | $0 | $10,000 |

| Borrow $5,000 from bank | +$5,000 | +$5,000 | — |

| Balance | $15,000 | $5,000 | $10,000 |

| Buy equipment for $3,000 cash | +$3,000 / −$3,000 | — | — |

| Balance | $15,000 | $5,000 | $10,000 |

Notice that in every single case, Assets ($15,000) = Liabilities ($5,000) + Equity ($10,000). The equation never breaks.

The Expanded Accounting Equation

As you advance, you’ll encounter the expanded form, which breaks equity into its components:

Assets = Liabilities + Owner’s Capital + Revenue − Expenses − Drawings

This expanded form shows exactly what drives changes in equity:

- Capital invested by the owner increases equity

- Revenue earned increases equity

- Expenses incurred decrease equity

- Drawings (money taken out by owner) decrease equity

The Accounting Equation in Financial Statements

The accounting equation is directly visible in the Balance Sheet — one of the four core financial statements. The left side of the balance sheet lists all assets, and the right side lists all liabilities and equity. Both sides must always be equal.

Key Takeaways

- The accounting equation (Assets = Liabilities + Equity) is the foundation of all accounting

- Every transaction affects at least two parts of the equation — keeping it balanced

- Assets are what you own; liabilities are what you owe; equity is what belongs to the owner

- The equation never breaks — if it does, an error has been made

- The expanded equation shows how revenue, expenses, and drawings flow into equity

Accounting Equation Practice Worksheet — Download, print, and complete to reinforce this lesson.