Debits and Credits: The Language of Double-Entry Bookkeeping

Every financial transaction has two sides. Double-entry bookkeeping records both sides of every transaction, ensuring the books stay in balance. This system, invented in 15th-century Italy, is still the global standard today.

The Core Rule

For every transaction, the total amount debited must equal the total amount credited. This is not optional — it is a mathematical identity. If your debits and credits don’t balance, an error has been made.

What “Debit” and “Credit” Actually Mean

Despite popular misconception, debit does not mean “money going out” and credit does not mean “money coming in.” The terms simply refer to the left side (debit) and right side (credit) of a ledger account called a T-account.

| Account Type | Increased by | Decreased by |

|---|---|---|

| Assets | Debit (Dr) | Credit (Cr) |

| Liabilities | Credit (Cr) | Debit (Dr) |

| Owner’s Equity | Credit (Cr) | Debit (Dr) |

| Revenue | Credit (Cr) | Debit (Dr) |

| Expenses | Debit (Dr) | Credit (Cr) |

Memory trick: DEAD CLIC — Debits increase Expenses, Assets, and Drawings; Credits increase Liabilities, Income, and Capital.

Journal Entries: Recording Transactions

A journal entry records a transaction chronologically. Each entry shows the date, accounts debited, accounts credited, and a brief description.

Example 1: You start a business by depositing $500,000 cash into the business bank account.

Dr. Cash (Asset ↑) $500,000

Cr. Owner’s Capital (Equity ↑) $500,000

Cash increases (debit); owner’s equity increases (credit).

Example 2: You buy office supplies for $8,000 cash.

Dr. Office Supplies Expense $8,000

Cr. Cash $8,000

Expense increases (debit); cash decreases (credit).

Example 3: You sell consulting services worth $25,000 on credit (invoice sent, not yet paid).

Dr. Accounts Receivable $25,000

Cr. Service Revenue $25,000

Asset (receivable) increases; revenue increases.

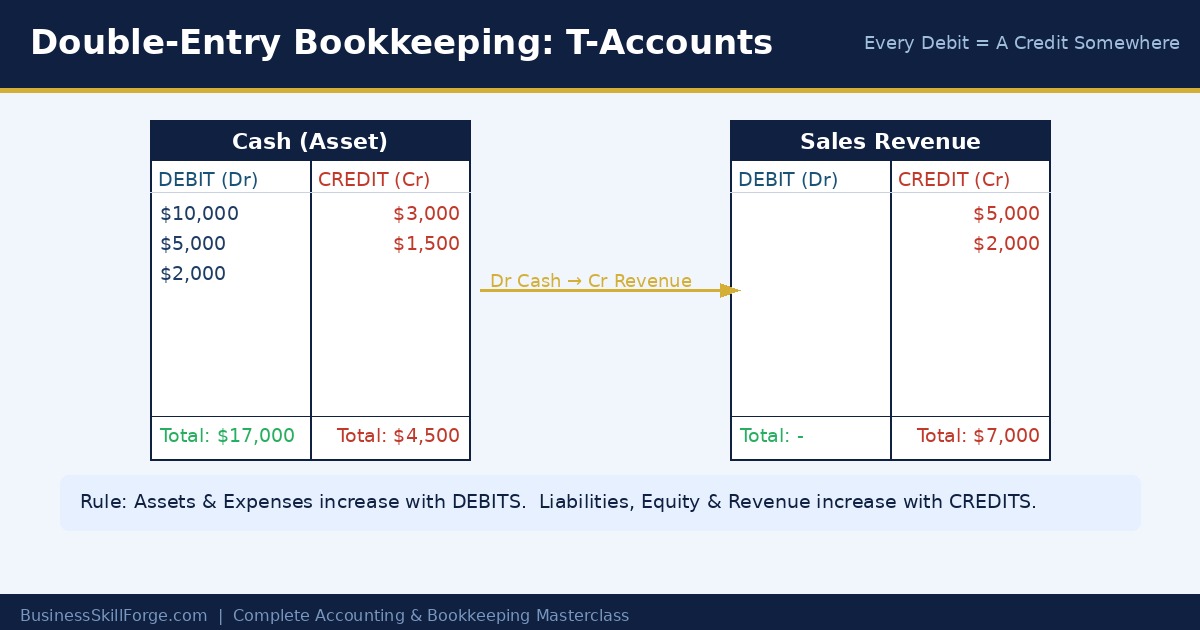

T-Accounts

A T-account is a visual representation of a ledger account with a left (debit) side and a right (credit) side. After posting all journal entries, the balance of each account is calculated by subtracting the smaller side from the larger side.

The Trial Balance

After posting all journal entries, a trial balance is prepared — a list of every account and its balance. The total of all debit balances must equal the total of all credit balances. A balanced trial balance is the first check that no mathematical errors have been made.

Lesson Summary

- Double-entry: every transaction has equal debits and credits.

- Assets and expenses increase with debits; liabilities, equity, and revenue increase with credits.

- Journal entries record each transaction in date order.

- The trial balance confirms debit totals = credit totals.

The Golden Rule: Every Transaction Has Two Sides

Double-entry bookkeeping was invented in 15th-century Italy — and it’s still the global standard today. The core insight is simple: every financial event simultaneously affects two accounts in equal and opposite ways. This is why accounting books always “balance.”

The confusion usually comes from the words debit and credit. Forget what you know from credit cards for a moment. In accounting:

| Account Type | Increases With | Decreases With | Memory Trick |

|---|---|---|---|

| Assets | Debit | Credit | Assets are what you OWN → Debits grow them |

| Liabilities | Credit | Debit | Liabilities are what you OWE → Credits grow them |

| Equity | Credit | Debit | Equity = owner’s claim → Credits grow it |

| Revenue | Credit | Debit | Revenue grows equity → Credits grow it |

| Expenses | Debit | Credit | Expenses shrink equity → Debits grow them |

Worked Example: 5 Transactions, Step by Step

Let’s record five real transactions for TechFix LLC, a small computer repair shop:

| # | Transaction | Account Debited | Amount | Account Credited | Amount |

|---|---|---|---|---|---|

| 1 | Owner invests $20,000 cash | Cash | $20,000 | Owner’s Capital | $20,000 |

| 2 | Buys repair equipment for $4,000 cash | Equipment | $4,000 | Cash | $4,000 |

| 3 | Earns $800 by repairing a laptop (cash paid) | Cash | $800 | Service Revenue | $800 |

| 4 | Pays $200 electricity bill | Utilities Expense | $200 | Cash | $200 |

| 5 | Buys $500 of parts on credit (accounts payable) | Parts Inventory | $500 | Accounts Payable | $500 |

After all five entries, total debits = $25,500 and total credits = $25,500. The books balance! This self-checking mechanism is one of the greatest features of double-entry accounting — errors are much harder to hide.

The T-Account: Your Visual Thinking Tool

A T-account is a simple visual that shows debits on the left and credits on the right. Here’s what the Cash account looks like after the transactions above:

| CASH | |

|---|---|

| Debit (+) | Credit (−) |

| $20,000 (owner invest) | $4,000 (equipment) |

| $800 (revenue) | $200 (electricity) |

| Balance: $16,600 | |

The balance is calculated as: $20,000 + $800 − $4,000 − $200 = $16,600

Debits and Credits Practice Worksheet — Download, print, and complete to reinforce this lesson.