The Balance Sheet: A Snapshot of Financial Position

The balance sheet (also called the Statement of Financial Position) shows, at a specific date, everything a business owns (assets) and everything it owes (liabilities), with the difference being the owners’ equity. It always satisfies: Assets = Liabilities + Equity.

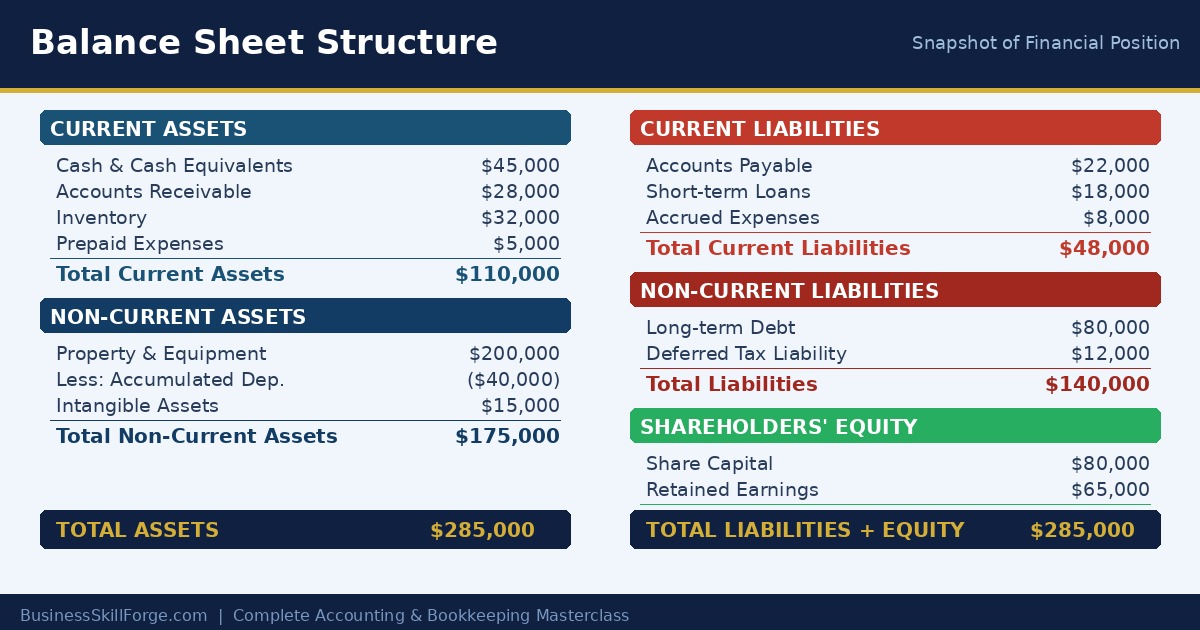

Structure of a Balance Sheet

Assets Section

Current Assets (expected to convert to cash within 12 months):

- Cash and cash equivalents

- Short-term investments

- Accounts receivable (net of bad debt allowance)

- Inventory

- Prepaid expenses

Non-Current Assets (held for more than 12 months):

- Property, plant and equipment (net of accumulated depreciation)

- Intangible assets (patents, trademarks, goodwill)

- Long-term investments

Liabilities Section

Current Liabilities (due within 12 months):

- Accounts payable

- Short-term borrowings

- Accrued liabilities (salaries payable, interest payable)

- Deferred revenue (current portion)

Non-Current Liabilities (due after 12 months):

- Long-term debt

- Deferred tax liabilities

- Pension obligations

Equity Section

- Share capital / Owner’s capital

- Retained earnings (accumulated net income minus dividends)

- Other comprehensive income (for listed companies)

Reading a Simple Balance Sheet

Bright Ideas Consulting — Balance Sheet as at 31 March 2025

ASSETS

Cash: $80,000 | Accounts Receivable: $120,000 | Equipment (net): $300,000

Total Assets: $500,000LIABILITIES

Accounts Payable: $60,000 | Bank Loan: $140,000

Total Liabilities: $200,000EQUITY

Owner’s Capital: $250,000 | Retained Earnings: $50,000

Total Equity: $300,000✓ $500,000 = $200,000 + $300,000

Key Things to Look for on Any Balance Sheet

- Current ratio (Current Assets ÷ Current Liabilities) — Can the business pay its short-term obligations?

- Debt-to-equity ratio — How much of the business is funded by debt vs. owners?

- Net asset value — Total Assets minus Total Liabilities = what owners actually own.

Lesson Summary

- The balance sheet is a point-in-time snapshot: Assets = Liabilities + Equity.

- Assets are classified as current or non-current; liabilities similarly.

- Key metrics derived: current ratio, debt-to-equity ratio, net asset value.

Balance Sheet Deep Dive: Assets, Liabilities, and Equity

The balance sheet is a snapshot — not a movie. It captures financial position at one moment, like a photograph. Understanding what belongs where is the foundation of financial analysis.

Current vs. Non-Current: The Key Distinction

| Category | Definition | Examples | Rule of Thumb |

|---|---|---|---|

| Current Assets | Converted to cash within 12 months | Cash, Accounts Receivable, Inventory, Prepaid Expenses | Listed in order of liquidity (cash first) |

| Non-Current Assets | Long-term, used over many years | Equipment, Buildings, Land, Intangibles, Goodwill | Shown net of accumulated depreciation |

| Current Liabilities | Due within 12 months | Accounts Payable, Accrued Expenses, Short-term Loans, Deferred Revenue | Pay with current assets |

| Non-Current Liabilities | Due beyond 12 months | Long-term bonds, Mortgage, Pension Obligations | Funded by long-term capital |

| Equity | Residual claim of owners | Common Stock, Retained Earnings, Additional Paid-In Capital | Always = Assets − Liabilities |

Full Balance Sheet Example: Meridian Software Inc. (Dec 31)

| ASSETS | $ | LIABILITIES & EQUITY | $ |

|---|---|---|---|

| Current Assets | Current Liabilities | ||

| Cash | 85,000 | Accounts Payable | 32,000 |

| Accounts Receivable | 48,000 | Accrued Wages | 8,500 |

| Inventory | 27,000 | Income Tax Payable | 6,000 |

| Prepaid Insurance | 4,000 | Short-term Bank Loan | 25,000 |

| Total Current Assets | 164,000 | Total Current Liabilities | 71,500 |

| Non-Current Assets | Non-Current Liabilities | ||

| Equipment | 120,000 | Long-term Loan | 80,000 |

| Less: Accum. Depreciation | (35,000) | ||

| Land | 50,000 | Total Non-Current Liabilities | 80,000 |

| Total Non-Current Assets | 135,000 | Equity | |

| Common Stock | 60,000 | ||

| Retained Earnings | 87,500 | ||

| Total Equity | 147,500 | ||

| TOTAL ASSETS | 299,000 | TOTAL L + E | 299,000 |

$299,000 = $299,000 ✓. Assets always equal Liabilities + Equity. If your balance sheet doesn’t balance, there’s an error — find it before presenting to investors or the bank.

Balance Sheet Practice Worksheet — Download, print, and complete to reinforce this lesson.