Why Financial Ratios Matter

A financial statement full of numbers doesn’t tell you much on its own. Is $500,000 in revenue good or bad? It depends. Financial ratios convert raw numbers into meaningful comparisons — letting you benchmark against competitors, track progress over time, and spot warning signs before they become crises.

Ratios are used by business owners, investors, lenders, and managers to answer questions like: “Can this company pay its bills?” or “Is it generating a good return?”

We organize ratios into four families:

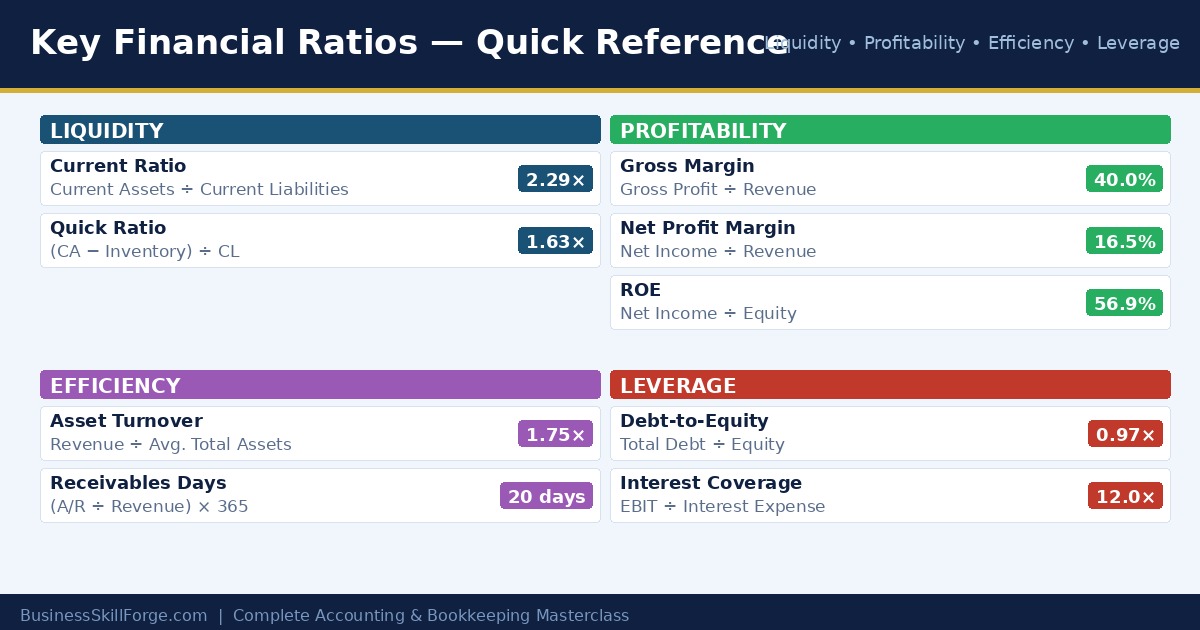

1. Liquidity Ratios — Can the Business Pay Its Short-Term Bills?

Liquidity ratios measure a company’s ability to meet obligations due within the next 12 months.

Current Ratio

Formula: Current Assets ÷ Current Liabilities

A current ratio above 1.0 means the company has more short-term assets than short-term debts. A ratio of 2.0 is generally considered healthy — it means for every $1 owed in the next year, the company has $2 available to pay it.

Example: Current Assets = $110,000 | Current Liabilities = $48,000

Current Ratio = $110,000 ÷ $48,000 = 2.29× ✓ Healthy

Quick Ratio (Acid-Test Ratio)

Formula: (Current Assets − Inventory) ÷ Current Liabilities

This is a stricter test. It excludes inventory because inventory can’t always be sold quickly. A quick ratio above 1.0 is generally comfortable.

Example: ($110,000 − $32,000) ÷ $48,000 = 1.63× ✓ Strong

2. Profitability Ratios — How Well Is the Business Making Money?

Gross Profit Margin

Formula: (Gross Profit ÷ Revenue) × 100

Shows what percentage of sales revenue is kept after paying the direct cost of goods sold. Higher is better. A 40% gross margin means for every $1 of sales, $0.40 is left to cover operating costs and profit.

Example: Gross Profit = $200,000 | Revenue = $500,000

Gross Margin = ($200,000 ÷ $500,000) × 100 = 40%

Net Profit Margin

Formula: (Net Income ÷ Revenue) × 100

The bottom line — what percentage of revenue becomes actual profit after ALL expenses, interest, and taxes.

Example: Net Income = $82,500 | Revenue = $500,000

Net Margin = ($82,500 ÷ $500,000) × 100 = 16.5%

Return on Equity (ROE)

Formula: (Net Income ÷ Shareholders’ Equity) × 100

Tells investors how efficiently the company is using their money to generate profit. A 15–20% ROE is typically considered good in most industries.

Return on Assets (ROA)

Formula: (Net Income ÷ Total Assets) × 100

Measures how efficiently the company uses all its assets to generate profit, regardless of how those assets were financed.

3. Efficiency Ratios — How Well Is the Business Using Its Resources?

Asset Turnover Ratio

Formula: Revenue ÷ Average Total Assets

Shows how many dollars of revenue are generated for each dollar of assets. A ratio of 1.75× means the company generates $1.75 in sales for every $1 of assets it holds.

Accounts Receivable Days (Debtor Days)

Formula: (Accounts Receivable ÷ Revenue) × 365

How many days on average it takes customers to pay. Lower is better — it means the company is collecting cash quickly. A figure of 20 days is excellent; over 60 days is a warning sign.

Inventory Turnover

Formula: Cost of Goods Sold ÷ Average Inventory

How many times the company sells through its entire inventory in a year. High turnover means strong sales and lean inventory management.

4. Leverage Ratios — How Much Debt Is the Business Carrying?

Debt-to-Equity Ratio

Formula: Total Debt ÷ Shareholders’ Equity

Compares how much the company is financed by debt versus owner investment. A ratio below 1.0 generally indicates conservative, manageable debt. Above 2.0 can signal high financial risk.

Interest Coverage Ratio

Formula: EBIT ÷ Interest Expense

Can the company comfortably pay its interest expense from operating profits? A ratio of 3× or above is generally considered safe. Below 1.5× raises serious concerns about solvency.

Example: EBIT = $120,000 | Interest = $10,000

Coverage = $120,000 ÷ $10,000 = 12.0× ✓ Very safe

Using Ratios Effectively

Ratios are only meaningful when used in context. Always:

- Compare over time — Is the current ratio improving or deteriorating year over year?

- Compare to industry benchmarks — A 5% net margin is terrible for a software company but excellent for a grocery store

- Use multiple ratios together — No single ratio tells the whole story; strong liquidity combined with weak profitability suggests a different problem than the reverse

Quick Reference Summary

| Ratio | Formula | Healthy Range |

|---|---|---|

| Current Ratio | Current Assets ÷ Current Liabilities | 1.5× – 3.0× |

| Quick Ratio | (CA − Inventory) ÷ CL | > 1.0× |

| Gross Margin | Gross Profit ÷ Revenue | Varies by industry |

| Net Margin | Net Income ÷ Revenue | > 10% is good |

| ROE | Net Income ÷ Equity | 15%–25% |

| Debt-to-Equity | Total Debt ÷ Equity | < 1.0 preferred |

| Interest Coverage | EBIT ÷ Interest | > 3.0× |

Key Takeaways

- Financial ratios convert raw numbers into comparable, actionable insights

- The four ratio families are: Liquidity, Profitability, Efficiency, and Leverage

- Always compare ratios to prior periods and industry benchmarks — never in isolation

- Strong liquidity + strong profitability = a financially healthy business

- High debt ratios with low interest coverage = a warning sign worth investigating

Financial Ratios Practice Worksheet — Download, print, and complete to reinforce this lesson.