The Cash Flow Statement: Following the Actual Money

A profitable business can still go bankrupt — if it runs out of cash. The cash flow statement reconciles net income with actual cash movements, revealing whether the business generates real cash or merely accounting profits. It is arguably the statement least easy to manipulate and most trusted by experienced analysts.

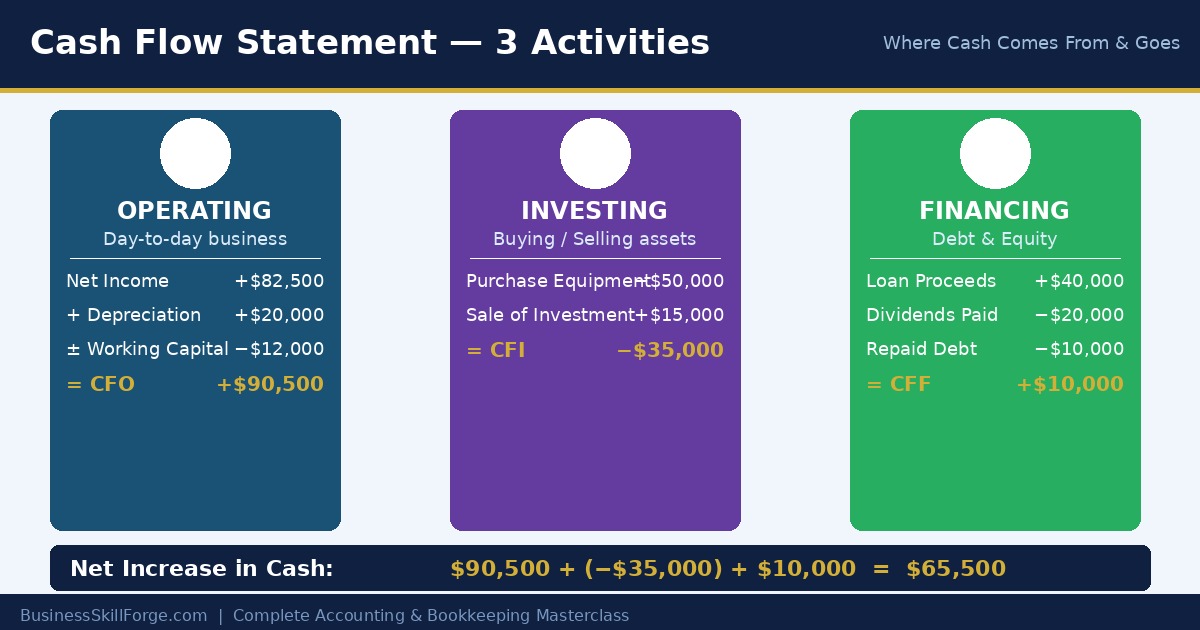

Three Sections of the Cash Flow Statement

1. Operating Activities

Cash flows from the core business operations — collecting from customers, paying suppliers, paying employees. This is the most important section: consistently positive operating cash flow means the business model actually works.

Two methods:

- Direct method — Lists each type of cash receipt and payment explicitly (cash received from customers, cash paid to suppliers, etc.). More transparent but rarely used in practice.

- Indirect method — Starts with net income and adjusts for non-cash items (depreciation) and working capital changes. Most companies use this method.

2. Investing Activities

Cash flows from buying/selling long-term assets and investments. Negative investing cash flow often signals growth (buying new equipment or acquiring companies). Persistently positive investing cash flow can signal asset sales — potentially a warning sign.

3. Financing Activities

Cash flows from raising and repaying capital — bank loans, issuing shares, paying dividends, buying back shares.

A Simple Indirect-Method Cash Flow Statement

TechFlow Solutions — Cash Flow Statement (Year ended 31 March 2025)

Operating Activities:

Net Profit: $750,000

Add: Depreciation: $150,000

Less: Increase in Receivables: ($200,000)

Add: Increase in Payables: $80,000

Net Cash from Operations: $780,000Investing Activities:

Purchase of Equipment: ($500,000)

Net Cash from Investing: ($500,000)Financing Activities:

Proceeds from Bank Loan: $300,000

Dividend Paid: ($200,000)

Net Cash from Financing: $100,000Net Increase in Cash: $380,000

Opening Cash: $420,000

Closing Cash: $800,000 ← Must match Cash on Balance Sheet ✓

Key Signals Analysts Watch

- Free Cash Flow (FCF) = Operating Cash Flow − Capital Expenditures. What remains after maintaining and growing the asset base. Companies with strong FCF can pay dividends, repay debt, or make acquisitions.

- Cash vs. Profit mismatch — If net profit is high but operating cash flow is low, profits may be driven by aggressive accruals. Investigate receivables and revenue recognition.

- Capex intensity — High capital expenditure relative to revenue signals asset-heavy businesses with ongoing reinvestment needs (manufacturing, telecoms).

Lesson Summary

- Cash flow statement has three sections: operating, investing, and financing activities.

- The indirect method starts from net profit and adjusts for non-cash items and working capital changes.

- Free Cash Flow = Operating CF − Capex; closing cash must match the balance sheet.

Three Sections of the Cash Flow Statement — In Detail

| Section | What It Covers | Positive = Good? | Example Items |

|---|---|---|---|

| Operating Activities | Cash from core business operations | Yes — means operations generate cash | Collections from customers, payments to suppliers, wages paid, tax paid |

| Investing Activities | Cash from buying/selling long-term assets | Not necessarily — can be growth investment | Purchased equipment, sold a building, bought securities |

| Financing Activities | Cash from debt and equity transactions | Depends — issuing shares is good; excessive borrowing is risky | Borrowed from bank, repaid loan, issued stock, paid dividends |

Full Indirect Method Cash Flow — Summit Outdoor Gear

| Operating Activities | Amount ($) |

|---|---|

| Net Income | 80,250 |

| Add: Depreciation (non-cash) | 12,000 |

| Add: Decrease in Accounts Receivable | 5,000 |

| Less: Increase in Inventory | (7,000) |

| Add: Increase in Accounts Payable | 3,500 |

| Net Cash from Operating Activities | 93,750 |

| Investing Activities | |

| Purchased new shelving and POS system | (45,000) |

| Proceeds from sale of old equipment | 8,000 |

| Net Cash from Investing Activities | (37,000) |

| Financing Activities | |

| Repaid bank loan | (20,000) |

| Dividends paid | (15,000) |

| Net Cash from Financing Activities | (35,000) |

| Net Increase in Cash | 21,750 |

| Opening Cash Balance | 25,000 |

| Closing Cash Balance | $46,750 |

Summit earned $80,250 profit but generated $93,750 in operating cash — actually more than profit because depreciation is non-cash. This is very common. The reverse is also possible: profitable companies with negative operating cash flow are in danger of insolvency. Always read operating cash flow alongside net income.

Cash Flow Statement Practice Worksheet — Download, print, and complete to reinforce this lesson.